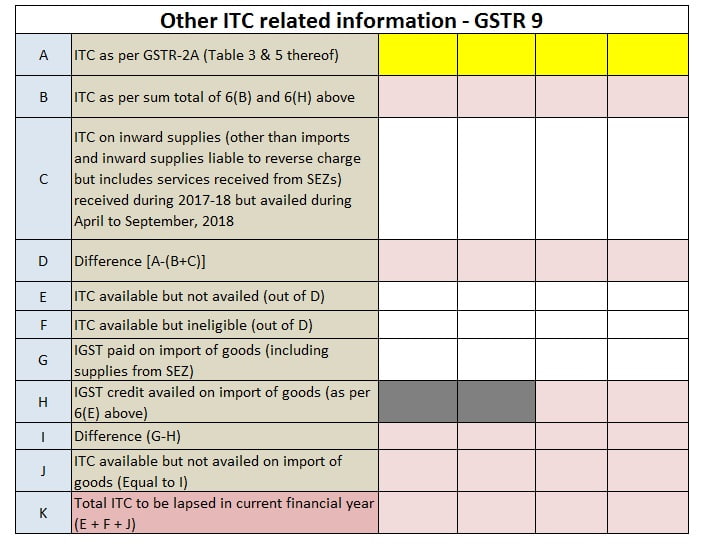

Other ITC Related Information GSTR 9

March 6, 2019

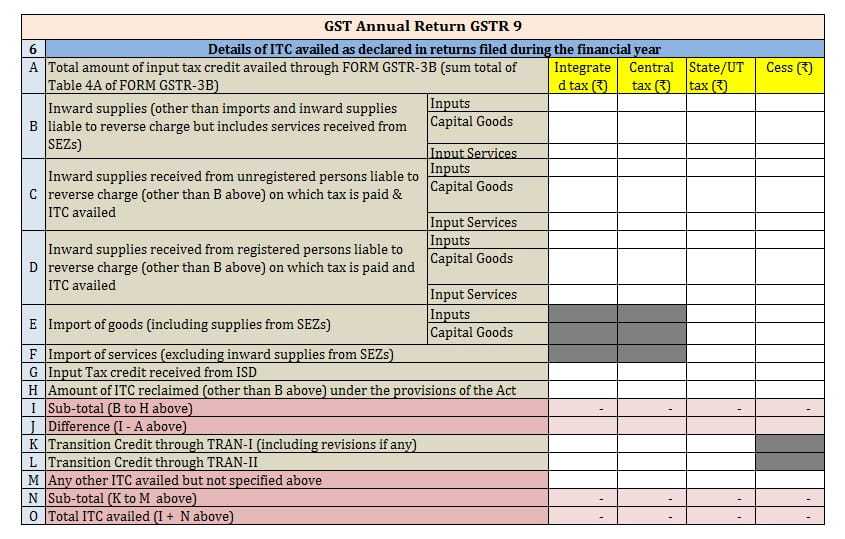

Details of ITC Availed during the Financial Year

March 7, 2019

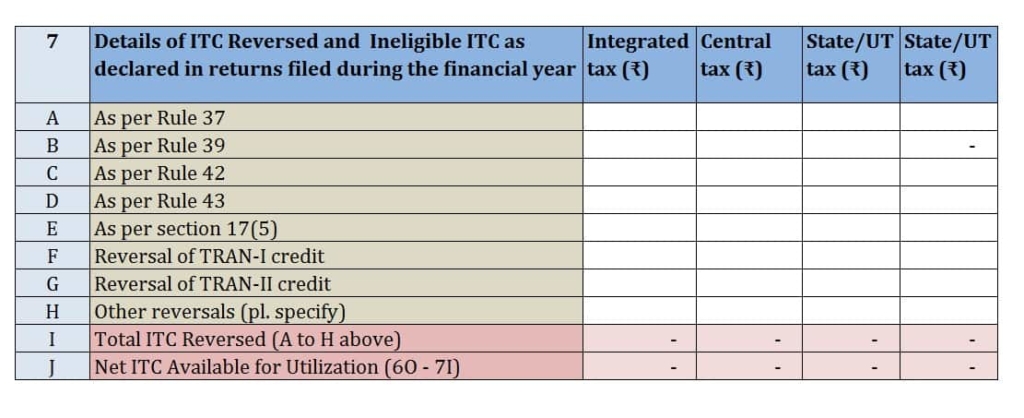

Under GSTR 9 Annual Return ITC Reversed and Ineligible ITC For Financial year is about reversal of GST Credit during the annual GST Return period. This section is about GST Credit reversal As per Rule 37, As per Rule 39, As per Rule 42, As per Rule 43, As per section 17(5). Also where GST Registered person who carried excess or ineligible credit in GST Trans return same also need to be revered in ITC Reversed and Ineligible ITC. Form GSTR 9 will automatically calculates amount of GST reversal applicable.

ITC Reversed and Ineligible ITC GSTR 9 Content

Content of ITC Reversed and Ineligible ITC under GST Annual Return

| 7 | Details of ITC Reversed and Ineligible ITC as declared in returns filed during the financial year | Integrated tax (₹) | Central tax (₹) | State/UT tax (₹) | State/UT tax (₹) |

| A | As per Rule 37 | ||||

| B | As per Rule 39 | – | |||

| C | As per Rule 42 | ||||

| D | As per Rule 43 | ||||

| E | As per section 17(5) | ||||

| F | Reversal of TRAN-I credit | ||||

| G | Reversal of TRAN-II credit | ||||

| H | Other reversals (pl. specify) | ||||

| I | Total ITC Reversed (A to H above) | – | – | – | – |

| J | Net ITC Available for Utilization (6O – 7I) | – | – | – | – |

ITC Reversed and Ineligible ITC Guidelines

- Details of input tax credit reversed due to ineligibility or reversals required under rule 37, 39, 42 and 43 of the CGST/SGST Rules, 2017 shall be declared here.

- This column should also contain details of any input tax credit reversed under section 17(5) of the CGST/SGST Act, 2017 and details of ineligible transition credit claimed through FORM GST TRAN-1 or FORM GST TRAN-2 and then subsequently reversed.

- Table 4(B) of FORM GSTR-3B may be used for filling up these details. Any ITC reversed through FORM GST ITC -03 shall be declared in 7H.

Related posts

March 9, 2019

March 7, 2019

{kind=link}