LLP Name Change Procedure

February 25, 2019

Private Limited Company Name Change

February 26, 2019

Payment of Tax Amnesty Scheme 2019 (Maharashtra Profession Tax)

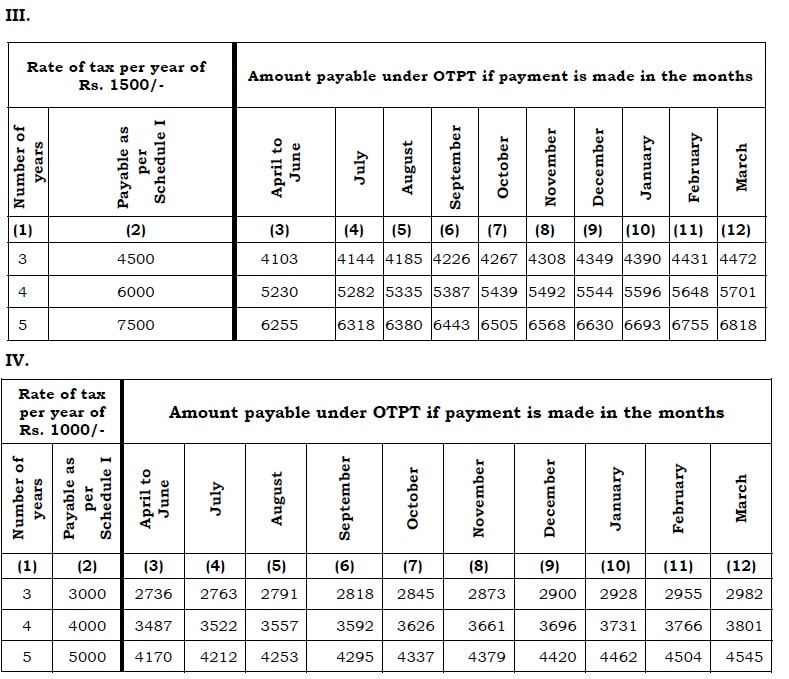

Maharashtra Government had introduced Professional Tax Amnesty Scheme form Professional Tax payment. This scheme is called as One Time Payment of Tax Scheme Professional Tax. Under this scheme concession will be given to dealers who will be making payment of old professional tax dues. Notification No. No. PFT.1218/C.R.52 is issued dated 22.02.2019. Under this scheme there are four Rate of taxes. Rs. 2500/- , Rs. 2000 , Rs. 1500 , Rs. 1000/-. Scheme have four table for identifying relief under Professional Tax.

Conditions to avail Scheme of Professional Tax Amnesty Scheme

- The person must be enrolled under the said Act.

- The enrolled person may opt the Scheme on the department’s website www.mahagst.gov.in at any time after his enrollment.

- Such enrolled person opting for the Scheme shall select the period for the Scheme as well as tax rate applicable to him and shall pay requisite amount as provided in the TABLE annexed to this Scheme.

- The Scheme shall be restricted to the period selected by an enrolled person. Such person may opt for the Scheme again after earlier period under the scheme is over. However the benefit can be availed at a time for a minimum period of three years upto a maximum period of thirty five years.

- The amount payable as per the TABLE shall be paid electronically.

- The enrolled person who has discharged his liability for payment of tax for a total continuous period of five years by making payment in advance of a lump-sum amount under provision of clause (a) of sub-section (3) of section 8 of the Act, prior to 1st April 2018, may also opt for the Scheme after completion of such period of five years

- The enrolled person who has already paid Profession Tax for the year 2018-2019 or has paid any lump-sum amount on or after 1st April 2018 for the periods starting from 1st April 2018, can also avail the benefit of Scheme by paying the balance amount payable for the period opted under the scheme as per the TABLE.

- If the enrolled person, who has availed the benefit of Scheme and has discharged his liability of Profession tax for a particular period, joins any employment during the period covered under the Scheme then, such person shall furnish to the employer ‘One Time Profession Tax Payment Certificate’ in Form A appended to this Scheme. In such case his liability to pay profession tax shall be restricted to the amount paid under the Scheme and the employer shall not be liable to deduct Profession Tax of the said person until completion of his period under Scheme.

- If the enrolled person has paid the Profession tax under the Scheme for a particular period and subsequently he is covered by any other entry having higher rate of tax than the rate applicable at the time of opting the scheme then, his liability to pay tax shall not be varied due to such change in the entry under Schedule I.

- Once the amount is paid under the Scheme, no refund of the amount paid shall be granted under any circumstances.

- If it appears that, the person has availed the benefit of the Scheme by suppressing any material information or particulars or by furnishing any incorrect or false information or, if any suppression of material facts, concealment of any particulars is found then the benefits availed under the Scheme shall be withdrawn. Such person shall be liable to pay tax at the rate specified in Schedule I of the Act.

FORM A

Professional Tax Amnesty Scheme

One Time Profession Tax Payment Certificate

[Under sub-section (3) of section 8 of the Maharashtra State Tax on Professions, Trades,

Callings and Employments Act, 1975]

Tax Payment Certificate No.

This is to certify that —————————– whose details are given below he is

enrolled person under the Maharashtra State Tax on Professions, Trades, Callings and

Employments Act, 1975.

- Enrollment Number –

- PAN –

- Name as per PAN –

- Trade Name –

- Schedule Entry –

- Address –

- Period covered under OTPT scheme – From ______ To ______

The holder of this certificate has discharged his Profession Tax liability for the period from———- to———. After completion of this period he will be liable to pay tax, if applicable, as per the provisions of the Maharashtra State Tax on Professions, Trades, Callings and Employments Act, 1975.

Place:

Digital Signature:

Date: ____________ Designation:

Download Optional Professional Tax Amnesty Scheme

Download Notification